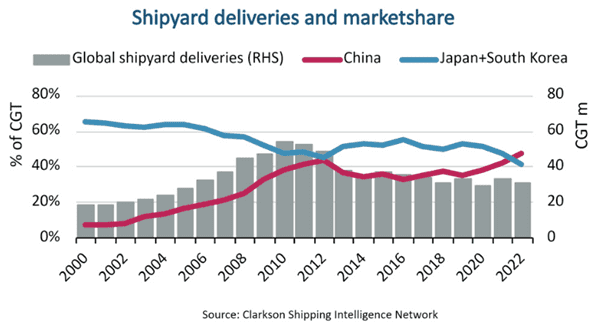

China’s shipbuilding industry is in a boom period and for the first time the shipyards exceeded the combined market share of Japanese and South Korean shipyards. The Chinese shipyards reached a hit record market share of 47% in 2022, according to market analysis of Bimco.

Ships delivered to new owners by Chinese shipyards in 2022 totalled 14.6 million Compensated Gross Tonne (CGT), a measure of shipyard activity, of the 30.8 million CGT delivered globally. The two other main shipbuilding nations, Japan and South Korea, delivered respectively 4.8 and 7.8 million CGT.

Twenty years ago, Chinese shipyards had a market share of less than 10% but a massive capacity expansion during the 2000s propelled the country to the number one spot already in 2009.

The shipyards in China also dominate the order book for ships to be delivered in the coming years. The global order book currently totals 109.1 million CGT, and 45% of those orders are held by Chinese yards compared to 34% and 10% by South Korean and Japanese yards respectively.

Chinese shipyards’ success has been achieved by maintaining a leading position within dry bulk ships and, more recently, establishing themselves as the premier location for building container ships. They also hold a large share of orders for most other ship types but have yet to establish themselves as key players within the gas carrier sector.

“LNG carriers are currently the second largest ship sector within the global order book for ships, and South Korean shipyards remain the market leaders within this sector, holding 79% of the order book,” in accordance with the analysis of Niels Rasmussen from Bimco.

In search of lower costs, countries like Vietnam and the Philippines could become larger competitors in the future, similar to how the centre of shipbuilding historically moved from Europe to Japan and onwards to South Korea and China.

Furthermore, Chinese shipyards hold only 15% of the LNG carrier order book, but they could make inroads also into this sector, just like they gradually attracted orders for ultra large container ships. However, in the short-term, yards in other countries are unlikely competitors and China, South Korea and Japan are likely to maintain their combined nearly 90% market share.

In accordance with the market analysis released, “in search of lower costs, countries like Vietnam and the Philippines could become larger competitors in the future; similar to how the centre of shipbuilding historically moved from Europe to Japan and onwards to South Korea and China.”

One of the latest deliveries is that of the bulk carrier “Seacon Nola” surveyed by the China Classification Society, and built by CSSC Huangpu Wenchong Shipbuilding Company Limited. Present to the delivery and naming ceremony on the 1st of February was the vice president of the China Classification Society, Fan Qiang.

The vessel is built by CSSC Huangpu Wenchong Shipbuilding Company Limited for Seacon Shipping Group Holdings Limited. It is the first of six 85,000-deadweight bulk carriers built by CSSC Huangpu Wenchong for Seacon Shipping Group Holdings Limited, which is classed by China Classification Society.

Source: Bimco and CCS